ARR Calculator: Free Calculator + Benchmarks (2026)

🎬 ARR Calculator walkthrough — why ARR is not just MRR times 12, the Net New ARR that tells the truth, NRR/GRR and Rule of 40 benchmarks, and why Upwork is the cheapest way for agencies to add new recurring revenue. Watch on YouTube

TL;DR

- ARR is not just MRR × 12. The strict definition counts only contracts of 12 months or longer, and it always excludes one-time fees, setup charges, and project work (ChartMogul, Wall Street Prep).

- The headline ARR number is the most-gamed metric in B2B. Counting bookings or signed multi-year deals as current ARR overstates it, sometimes by 2–3×.

- Net New ARR = New + Expansion − Contraction − Churn. ARR can climb while the business decays, because new logos mask the leak underneath.

- Read ARR next to retention: median private-SaaS NRR sits around 100–105% and good GRR is 85–90% (SaaS Capital). The Rule of 40 (growth % + margin % ≥ 40) is the single sanity check that ties it together.

- The calculator below turns your starting ARR and your four movement numbers into Net New ARR, ending ARR, growth rate, NRR, GRR, and a Rule of 40 score, each graded against 2026 benchmarks.

The fastest way to fail due diligence is to quote an ARR number the buyer then recomputes and cuts in half.

It happens because "ARR" gets used for three different numbers, and the flattering one is the easiest to say out loud.

I have watched a founder pitch "$2M ARR" that turned out to be roughly $1.1M of recurring software plus a pile of one-time onboarding fees and one signed three-year deal counted in full. The recurring base was real, but the headline was fiction.

ARR is only useful when you compute the recurring part honestly, then read it next to the two numbers that decide whether it survives the year: Net New ARR and net revenue retention.

This guide gives you the exact formulas, the strict-versus-run-rate distinction acquirers actually use, the 2026 retention and growth benchmarks, and a calculator that scores all of it in one pass.

Interactive Tool

ARR Calculator

Enter your starting ARR and the four movements that changed it this year. Get Net New ARR, ending ARR, growth rate, NRR, GRR, and a Rule of 40 score, each graded against 2026 benchmarks.

What ARR actually is, and why MRR × 12 is the lazy version

Annual Recurring Revenue is the annualized value of the revenue you can contractually count on repeating. The catch is that there are two legitimate definitions, and they do not always agree.

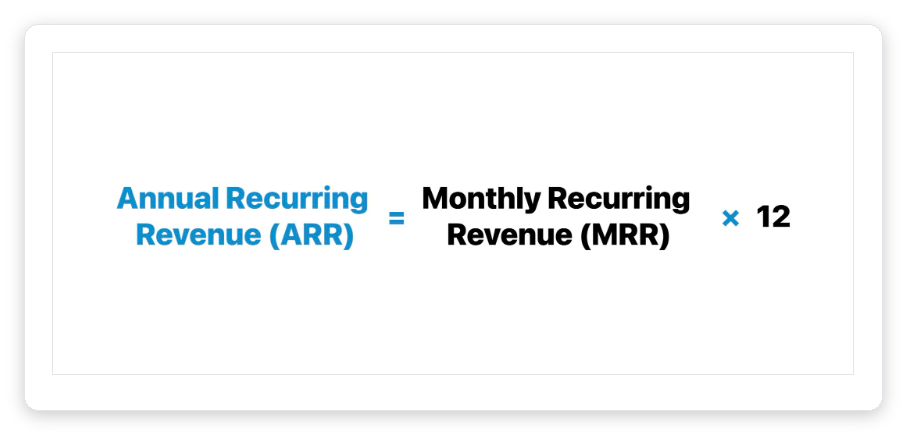

The first version, MRR × 12, is what most people mean when they say ARR. ChartMogul calls this the Annualized Run Rate, the most popular usage, and it includes monthly contracts because it simply scales your current monthly base up to a year.

The second version is stricter. ChartMogul's true "Annual Recurring Revenue" counts only contracts with a service length of 12 months or more and discards everything shorter, which is why a healthy book of month-to-month deals can be large in run-rate terms and zero in strict-ARR terms.

One-time fees never count: Wall Street Prep and Software Equity Group are blunt that setup fees, professional services, onboarding, and installation are all non-recurring and must be stripped out. Leave them in and a business with $5M of real recurring revenue reports $6M, a 20% overstatement that surfaces in the first diligence call.

There is also a third number people confuse with ARR: Contracted ARR (CARR), the annualized value of every signed contract including ones that have not started yet. CARR is a useful backlog metric, but it is not your current ARR, and quoting it as ARR is the single most common inflation move.

Net New ARR is the number that tells the truth

Total ARR going up feels like winning. It can also hide a business that is quietly leaking, because a growing new-logo number papers over churn underneath it.

That is why operators who know the metric watch Net New ARR instead. It nets every movement against each other in one figure.

The four components come straight from Wall Street Prep's breakdown of ARR movement and MetricHQ's Net ARR Added formula.

MetricHQ calls Net New ARR the single most important metric for understanding subscription health, precisely because gross "new ARR" alone can look great while the net effect is flat.

New ARR from first-time customers, plus Expansion ARR from existing customers buying more.

Contraction ARR from downgrades, plus Churned ARR from accounts that left entirely.

A team books $1M of new ARR and celebrates, while $700K churns and contracts away the same year. Net New ARR is $300K, not $1M, so reporting only the top half just funds acquisition to outrun a retention problem you never named.

NRR and GRR decide whether your ARR grows while you sleep

Net New ARR tells you what happened this year. Net revenue retention tells you what your existing customers will do next year with no new sales at all.

SaaS Capital defines NRR as this year's recurring revenue from last year's customers, divided by what those same customers paid last year. It includes expansion, so it can run well above 100%.

Gross revenue retention uses the same base but strips out expansion, so it can never exceed 100%. It answers a colder question: how much of last year's revenue would survive if nobody upgraded.

NRR above 100% means your existing base grows on its own. NRR below 100% means you have to win new ARR every year just to stand still, and that is a treadmill most agencies know intimately.

| Retention band (2026) | NRR | GRR | Read |

|---|---|---|---|

| Top quartile | 110–120%+ | 90–95%+ | Base compounds without new sales |

| Median (mid-market) | 100–105% | 85–90% | Healthy, expansion offsets churn |

| Small-customer / SMB | 90–100% | 80–88% | Treadmill: new ARR replaces losses |

| Below the line | < 90% | < 80% | Leaking faster than you can sell |

These ranges track SaaS Capital's retention data, where companies with $25K–$50K contracts show a median NRR around 102%, and Benchmarkit's 2025 figures putting good GRR in the high 80s to low 90s. Below-the-line retention is the most expensive problem in the business, and it never shows up in a total-ARR chart.

The growth-rate and Rule of 40 benchmarks almost nobody hits anymore

Once your ARR and retention are honest, the next question is whether your growth rate is any good for your stage. The bar has dropped hard since the zero-rate boom.

KeyBanc's 2025 private-SaaS survey reports expected year-over-year ARR growth rising from 15% in 2024 to 20% in 2025, the first uptick in three years. That is the new normal, not the 100%+ that founders still quote from memory.

| Stage | Realistic ARR growth | Note |

|---|---|---|

| Under $5M ARR | 50–60%+ | Small base, strong PMF still triples in good years |

| $5M–$20M ARR | 30–50% | Law of large numbers starts to bite |

| Above $50M ARR | 20–30% | Strong if margins are healthy too |

| Agency / services on retainer | 10–25% | Labor-bound, so retention matters more than speed |

The famous T2D3 path (triple, triple, double, double, double to $144M ARR) still exists, but Battery's own framing treats it as a best case for venture-backed hypergrowth, not a benchmark for the median company. For a services business it is essentially unreachable, and chasing it is how agencies torch margin.

Five ways B2B teams inflate ARR and get caught in diligence

Each of these makes the number look bigger and the business look healthier than it is. They are ordered by how often I see them blow up a deal or a board update.

- 1 Counting bookings or CARR as current ARR. A signed three-year, $900K deal adds $300K to ARR per year once it goes live. Counting the full $900K, or counting it before it starts, is the most common overstatement there is.

- 2 Baking one-time fees into ARR. Setup, onboarding, migration, and professional services are non-recurring by definition. Fold them in and your recurring base looks larger and your retention math breaks.

- 3 Reporting only new and expansion, ignoring contraction. Celebrate the additions, bury the downgrades and churn, and Net New ARR looks like gross new ARR. The gap is exactly the part that predicts next year's trouble.

- 4 Over-annualizing unstable monthly revenue. A one-month usage spike multiplied by 12 becomes a fake ARR jump. Annualize only revenue with real renewal behavior, and label volatile or seasonal income as run rate, not ARR.

- 5 Mishandling discounts. Report ARR at the discounted year-one price, then forget to update it when the discount rolls off or renews. Ordway flags discount normalization as one of the quietest sources of ARR drift.

Do agency retainers count as ARR? Yes, but only the part that renews

Agencies increasingly report ARR, and they are right to. A contractually committed monthly retainer that renews behaves exactly like a subscription for forecasting and valuation.

The discipline is the same one SaaS teams need: only the recurring portion qualifies. A retainer that renews on a defined cadence is ARR, while the one-off campaign, the project build, and the pass-through ad spend are not.

A marketing agency on $85K/month of true retainers might bolt on a $40K one-time website build and quote it all as recurring. That inflates ARR by nearly half and collapses the moment the project ships, which is why you segment retainer revenue from project revenue and count only the renewable part.

For agencies the retention numbers bite harder than the growth numbers. With commoditized, short retainers it is hard to hold NRR above 100%, which makes a steady supply of new retainer clients the difference between compounding and standing still.

That is where the acquisition channel you choose matters more than the spreadsheet. The mechanics of holding existing accounts live in our notes on client retention strategies, and the monthly view sits in the MRR calculator.

Why Upwork is the cheapest way to add Net New ARR

If new retainer logos are what move agency ARR, the real question is which channel delivers them at the lowest fully-loaded cost. Most outbound channels are expensive precisely because you are creating demand from scratch.

Upwork inverts that: the client already has budget, already has intent, and already posted the job. You are answering demand, not manufacturing it, which is why marketplace ARR tends to land cheaper than paid or SDR-driven pipelines (the channel-cost math sits in our CAC calculator).

The intent shows up in the response data. GigRadar's pipeline data for May 2026 shows an overall reply rate of 5.8% across 67,600 outbound agency proposals, rising to 8.7% in Sales & Marketing (n = 13,583).

Against paid channels where a 1–2% lead-to-reply rate is normal, that intent is the whole edge. New-logo ARR only stays cheap, though, if your proposal volume stays predictable, and manual bidding is the first thing that slips the week delivery gets busy.

That is the exact gap GigRadar closes. We operate a real Upwork Business Manager account.

Your agency invites our BM through Upwork's official invitation system, the same role you would use to onboard a hired bidder. Proposals submit from our BM under our team's supervision, your own freelancer account is never touched, and if Upwork ever reviews a submission, the review lands on our BM profile.

The result is a steady top-of-funnel of payment-verified, intent-rich clients feeding the New-ARR line, at a cost most outbound motions cannot match. The model is broken down in our guide to Upwork automation.

Free for Upwork agencies

Feed your New-ARR line on autopilot

We run an Upwork Business Manager that submits proposals on your agency's behalf, so new-retainer ARR stops depending on whoever remembered to bid this week. Get a free audit of your pipeline.

Get Your Free Agency Audit →Run your real numbers

The fastest way to know whether your ARR is healthy is to stop quoting one big number and split it into the four movements that made it.

Then ask the cheaper question: which channel adds new-logo ARR at the lowest fully-loaded cost? For most Upwork agencies, the marketplace beats every outbound line they run, and pairing that with disciplined value-based pricing lifts the retention side at the same time.